On 12.03.2025, Trump has announced a 25% tariff on imports of steel and aluminium products. This will mainly affect Canada, as 23% of US steel imports and 58% of aluminium imports come from its northern neighbour. As producers will try to pass on this impact to consumers, this will certainly lead to a price increase, which is likely to lead to a renewed surge in inflation. This will cause turbulence in the equity markets, and it is unpredictable at this stage what the impact of a renewed surge in inflation will be on economic growth. At the same time, it could put domestic steel producers in an interesting position, as their products will cost relatively less than those of foreign competitors, which could lead to higher sales volumes and, on a like-for-like margin, higher profits. My analysis looks at one of the largest US steel producers, Steel Dynamics. As I mentioned above Steel Dynamics is one of the largest steel and metal processing companies in the world and the US, with a steel production capacity of 13 million tonnes and the largest producer of carbon-based steel products in the US. It is one of the most efficient steel producers in terms of production, profit margin and operating profit. Since its founding in 1996, it has acquired a large number of companies to become a huge conglomerate.

Financial Overview

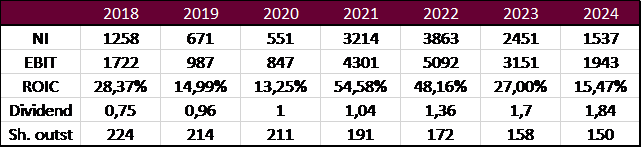

The company’s Net Income and EBIT are volatile, in the period of 2021-2023 doing exceptionally well, while in 2019-2020 is weaker. However, if we look at the return on invested capital, it is always between 15% and 28% (excluding some extraordinary years), averaging around 20% per year. This is excellent for a heavy industrial company. The company has steadily increased its dividend over the past seven years, with a current dividend yield of 1.5% based on a share price of $125. It has a significant share buyback activity, reducing its shares outstanding by 33% over seven years, this is an another form of shareholder return at the company.

FCFF valuation

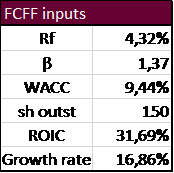

Using the 10-year U.S. Treasury bond as the risk-free rate, the weighted average cost of capital (WACC) is 9,44%. The average Return on Invested Capital (ROIC) over the past five years was 31,69%. Since the ROIC exceeds the WACC, the company is considered a value creator. Taking into account the reinvestment requirements, the growth rate of Free Cash Flow to Firm (FCFF) is 16,86%, which is a substantial growth rate for a mature company.

Based on the FCFF valuation, the intrinsic value of the company’s stock is $175,15, 40% higher than the current price of $124,94. This suggests that the stock is significantly undervalued. If we calculate with a 30% margin of safety, our target price will be $122,6, which is close to the current price. This means that at the current price we should buy this company, because of the stock is undervalued.

Assuming that Steel Dynamics’ will have a favourable athmosphere compare to its foreign competitors as a result of the tariff policy, and that it will therefore be able to sell in higher volumes and thus earn higher profits in the coming years, the calculated enterprise value assumes a very conservative valuation.

Relative valuation

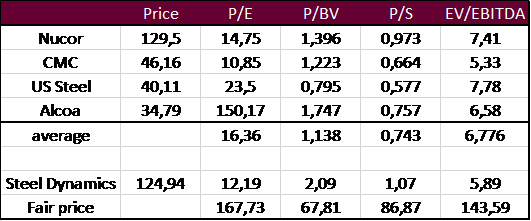

The relative valuation takes into account the price and value performance of four other competitors. These companies are all active in the US and are therefore easily comparable. Nucor (NUE), U.S. Steel (X), Alcoa (AA), and Commercial Metal (CMC) are all domestic competitors of Steel Dynamics (STLD). It can be seen that the share prices of competing companies have followed quite different paths over the past year and a half. While Steel Dymanics has risen nearly 20%, there have been steel companies that have risen even more (Alcoa or U.S. Steel), but there have also been some that have fallen more than 10%. Overall, the average 15% rise in share prices lags behind the 34% rise in the S&P500 stock index over the past year and a half.

Relative valuation shows whether a company is over- or undervalued compared to its competitors, based on indicators. Due to the low net income of Alcoa and US Steel in 2024, we obtain high P/E values, Alcoa’s value is not taken account into the calculation. Due to the fact that Alcoa’s price has increased by more than 30%, its P/B ratio is above average, and we do not see high values for US Steel despite the increase in its share price. Although the shares of competitors have had different price movements, the sector is moving quite together based on the metrics. Based on the relative valuation, the resulting target price ranges from $67,8 to $167,73, with an average of these prices of $116,5. Since the price is $124,94, the company is correctly valued compared to its competitors.

Summary

Steel Dynamics Steel was valued using the FCFF DCF method. Based on this, the company is undervalued, with the current price 40% lower than the intrinsic price of $175,15. Including a margin of safety, I am making a buy recommendation at the current price of $124,94. Based on relative valuation, the company is fairly valued, if the tariffs will be in place, the domestic producers will benefit from this situation so buying this company should have been beneficial in the longer term.